JOHANNESBURG (miningweekly.com) – The underpinning of platinum group metals (PGM) prices by investment and speculation is expected to persist for as long as the high level of macro uncertainty persists, Sibanye-Stillwater executive VP sales and marketing Kleantha Pillay spelt out at the company’s Capital Day in Helsinki, Finland, on Monday, April 20.

“If we shift a bit into a longer or medium term, primary supply is forecast to decline from around the 6.2-million ounces a year pre-Covid level of 2019 down to 4.7-million ounces a year by 2034 – and this reflects the years of under investment into South African supply as producers navigated a number of operating challenges, including cost inflation, crime, water, power.

“The decline in palladium supply from 6.8-million ounces pre-Covid to 5.6-million ounces a year in 2034 is somewhat slower than it is for platinum, as we've got Platreef and some Russian expansion coming online over the next ten years.”

On secondary supply, Pillay added: “We do expect to see some recovery in secondary supply. However, we model recoveries at similar rates to what we have seen historically.

“Combining secondary supply recovery and the primary supply forecast, we actually see total platinum supply declining 1.4% per year from the highs of 2019, where palladium supply declines a bit slower at 0.6% per year over the same period, so the recovery in secondary supply does not offset the decline in primary supply,” Pillay outlined during the event covered by Mining Weekly.

PRETTY ROBUST DEMAND

“On the demand side, we're just looking at our biggest demand sector, which is autocats, and we see the outlook for catalysed vehicles, so that's internal combustion engine (ICE) vehicles and ICE hybrids, remaining pretty robust over the next ten years.

“Since 2023 and the peak of the battery electric vehicle (BEV) hype, global data has been revising its battery electric forecast downwards each quarter, reflecting what I think are more realistic growth rates as well as some shifts in regulation and purchase incentives.

“The recent easing of the European emissions targets provides a boost for catalysed vehicles for longer, while US Federal incentives for BEVs expired in September last year. There are limited local government and OEM incentives remaining in place for battery vehicles in the US.

“In China, incentives have shifted from a flat rate to price-based incentives, so we do expect to see some downside risk for smaller, cheaper models, and that's across all power trains.

“Our house view of BEV growth has always been a bit more tempered, and that remains the case now.

“The current market view expects 42% battery electric vehicle market share by 2034 so that's a growth rate of 12% per year from now for the next ten years.

“Our more tempered view is 35% BEV market share by 2034, which still implies a fairly aggressive growth rate of 9% per year for the next ten years.

“There is some downside risk to overall vehicle production numbers in the next year or so as macro factors such as inflation weigh on affordability. This, of course, translates into some downside risk on secondary supply as well as fewer vehicles being scrapped,” Pillay reported.

Putting together Sibanye-Stillwater’s supply and demand views, the ten-year forecast of this Johannesburg Stock Exchange-listed company includes two assumptions which the company differs from the market on.

“The first is our view on market penetration for battery vehicles, which we've just talked through and the second is around recycling.

“Our view is that recycling is going to revert to historical recoveries and what that means over a nine-year period is that our recycling view is four-million ounces lower than the market views, and that is on a 3E basis.

“I also want to point out that we don't include investment demand in our forecasts, so our 2025 balances for platinum and palladium include a change in investment holdings.

“However, we do believe investment demand has a role to play in providing some additional balance to these metals.”

Regarding platinum, deficits through the forecast period are foreseen with some investment ounces coming back to market at the right prices.

Regarding palladium, the gradual decline in the gasoline autocat demand numbers is reflected in the forecast, with the market moving into balance around 2029 and then into modest surpluses.

“Because platinum and palladium are largely substitutable, we also look at this on a 2E balance basis, and again showing, I think, a fairly constructive outlook over the period, excluding changes to investment demand.

“Our outlook for rhodium pretty much mirrors that for palladium, just given its primary use in autocats as well,” Pillay outlined.

FILLING IN BEYOND 2034

“If we look out beyond 2034 for more as BEVs continue to grow and catalysed vehicles continue to fall, we can't really count on any single application to fill this gap.

“By 2034, we are expecting just under a million ounces of 6E demand for hydrogen and fuel cells, and that would be across applications like fuel cell electric vehicles, stationary fuel cells, PEM electrolysers and membranes for hydrogen purification.

“We do expect this to grow beyond the 2034 period. We can't, however, bank on this completely, and we therefore continue to collaborate with various partners and fabricators to make sure that we're investing to create new applications that better match demand with the basket of supply.

“Our preference has always been for more sticky industrial demand and these are a few of the projects that we're working on now.

“Our electrolyser catalyst project with Heraeus has focused on replacing iridium with ruthenium in a traditional iridium oxide electrolyser catalyst.

“This would not only allow for a more cost-effective catalyst but would also make use of a less scarce metal and both of these things provide more confidence to OEMs, and to users, that PEM electrolysers can be a sustainable technology to invest in.

“We also announced two new projects last week.

"Bushings for the production of glassfibres were traditionally a platinum-rhodium alloy, which is very suitable for these high temperature applications.

“With rhodium prices moving above the $30 000/oz level a few years ago, OEMs had largely thrifted out the rhodium and replaced it with platinum.

“We're now working with Heraeus to substitute platinum with palladium in this application, which again, should result not only in a more cost-effective product, but also then help absorb some of the palladium supply,” Pillay reported.

NUCLEAR ENERGY CORPORATION OF SOUTH AFRICA

Moreover, Sibanye-Stillwater is collaborating with the Nuclear Energy Corporation of South Africa to develop a radioactive palladium isotope, which is derived from rhodium and is used largely for targeting and treating cancerous tumors.

This is early-stage research and development to understand the economic feasibility of the production of this isotope.

“This is not going to lead to huge amounts of rhodium demand, but this really has the potential to improve the quality of lives.

“Then, together with Valterra Platinum and Johnson Matthey, we've kicked off a three-year programme to identify, evaluate, develop and commercialise PGM-based applications.

“This kicked off in February and so the early part of the collaboration will focus on originating opportunities that we can develop further.

“Just to wrap up, the short-term dynamics of PGMs are driven by tariff threats and geopolitics, which are going to continue to impact on global growth and volatility in the short term.

“Our medium-term outlook remains constructive, characterised by stronger catalysed vehicle demand with a long tail, declining primary supply profile and very modest supply recovery support.

“Longer term we're positive on growth in the hydrogen market, but that said, the industry does need to invest in new applications for PGMs, and we continue to look for suitable opportunities in the hydrogen space,” Pillay added.

HYDROGEN IN SOUTH AFRICA

During question time, Mining Weekly put these questions:

Mining Weekly: In China, it has been reported that trucks are being powered by grey hydrogen on a growing scale, with steps being taken to convert to green hydrogen by 2030. South Africa's Sasol has been producing grey hydrogen since 1950. How, in your view, can South Africa Inc. begin to introduce mobility with grey hydrogen and then move to green hydrogen in the heavy vehicle and large South African taxi business in particular. What sort of lead needs to be taken in South Africa, in your view?

Pillay: All good points and I think there is a lot of work being done at the moment locally on looking at dual fuel and fuel cell applications. I think with China, as you mentioned, China got this right. They decided they wanted to do it, so they put the incentives in place to make sure that people would use it, and they also helped build up the infrastructure, so the refueling stations. I think the challenge we have here is that if something is not cost efficient, or does not have a cost advantage over the current technology, and there's no infrastructure build out, it's very hard to get big users or fleet users to make that change. I would love to see this happening here as well, but it really needs a kind of incentive that the Chinese would have rolled out that made this work in China, and that's really what we need to get it going.

Mining Weekly: Would it be beneficial, in your view, for regions to have their own PGM exchanges for buying and selling PGMs?

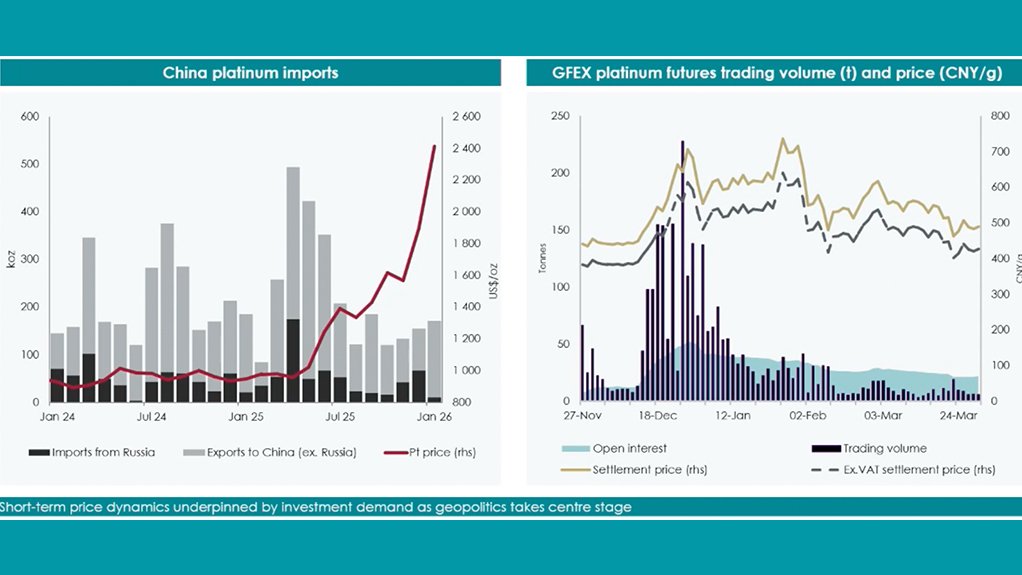

Pillay: We already have that to a large extent. In China, you've got the Shanghai Metals Exchange, and now you've got the GFEX. In the US, you've got COMEX and NYMEX, and then you've got the LBMA markets in London, so we're already seeing that to a large extent and if you have a look at how those three different regions behave, you can already see a bit of dislocation or difference in where demand is coming from at different times. But this is largely a metal that is very much global, it's fungible, and it’s very easy to move around the world, so I don't see much need to have more exchanges than that. It's really easy to fly this metal around the world. I would probably think we're well covered for now.

EMAIL THIS ARTICLE SAVE THIS ARTICLE ARTICLE ENQUIRY FEEDBACK

To subscribe email subscriptions@creamermedia.co.za or click here

To advertise email advertising@creamermedia.co.za or click here