JOHANNESBURG (miningweekly.com) – South Africa’s non-integrated chrome ore exporters want to discuss ways of solving the existential threat to South Africa’s struggling ferrochrome industry to avoid the need for a tax being imposed on the export of locally mined chrome ore.

But steadfastly in favour of a chrome ore export tax are South Africa’s ferrochrome industry spokespersons, who fully support the October 22 announcement of the Minister in the Presidency, Jackson Mthembu, that the Cabinet has proposed that a tax be imposed on the export of chrome ore from South Africa. (Also watch attached Creamer Media video.)

Currently 84% of cross-border chrome ore is exported from South Africa, with lower-percentage participants including Turkey at 9%, Albania at 3%, Pakistan at 2% and rest-of-world countries at another 2%.

ChromeSA representatives David Kovarsky, Phoevos Pouroulis and Alistair McAdam presented a collective suggestion to Mining Weekly in a Zoom interview that the stuggling ferrochrome industry should be given a special electricity dispensation rather than export tax protection.

But they cannot say much beyond that as they are not legally permitted to enter into holistic discussion on additional solutions until they receive an applied-for but not-yet-granted exemption to do so from the Competition Commission.

In the meantime, ChromeSA’s firm collective belief is that an affordable electricity tariff would allow the ferrochrome industry to regain the market share it has lost.

“The benefit of a chrome ore tax is just going to be whittled away by increasing electricity tariffs,” Kovarsky, a seasoned former ferrochrome producer, who now speaks on behalf of chrome ore exporters, contended.

“Introducing a tax will not, in the longer term, give ferrochrome any benefit at all. It’s like prescribing the wrong medicine for an illness,” McAdam, also a former ferrochrome executive of long standing, concurred.

And even if an export tax on chrome ore were imposed as a temporary measure, the damage to the non-integrated chrome ore mining companies would be permanent and result in job losses, Pouroulis warned.

But the ferrochrome industry expresses strong views in the exact opposite direction: “We need temporary relief in the form of a tax to survive,” Richards Bay Alloys CEO Andries van Heerden emphasised in a written response to Mining Weekly.

ChromeSA’s contention that significant volumes of South African chrome ore would be displaced with supply from other sources were fundamentally wrong, Van Heerden contended.

"China cannot simply replace South African ores. There are no economically viable sources of chrome ore internationally that can replace the volume of South African ore,” he said. Also supporting the imposition of a tax on the export of chrome ore are:

- South Africa’s six other ferrochrome producing companies, which consume 8.2-million tonnes of chrome ore a year, employ 6 851 people directly, support 68 000 jobs overall, contribute R41-billion to South Africa’s gross domestic product (GDP), pay R14-billion a year to Eskom, have pay-as-you-earn tax payments of R1.4-billion, buy 2.5-million tonnes of product a year from 20 South African reductant mines, and accord R42-million a year in social support and local enterprise development;

- the 1 177-employee Tendele Coal Mining, along with another five South African anthracite producers, which collectively provide jobs for another 3 800 employees; and

- the 1 500-employee Columbus Stainless of Mpumalanga, which produces stainless steel locally from the locally produced ferrochrome.

Already five of South Africa’s ferrochrome smelters have either been shut down, liquidated or placed in business rescue. These smelters supported more than 31 000 jobs along with a yearly contribution of R11-billion to South Africa’s GDP.

Direct employment lost in the past five years totals 1 139 jobs. Another 1 608 jobs are currently at risk under Section 189 of the Labour Relations Act, and remaining at risk are another 5 243 jobs.

“We might not have all the answers for the ferrochrome business, but we do have some ideas that can assist, but we need the Competition Commission to give us that exemption. We have the Genesis report. It’s very good work, but we’ve not been engaged with on this by government. Essentially, they just continue to move ahead without us,” said McAdam.

MINERALS COUNCIL SOUTH AFRICA

Minerals Council South Africa, the key role of which is to facilitate interaction among mining employers to crystallise desirable industry standpoints, represents both ferrochrome producers, who favour the imposition of an export tax on chrome ore, and chrome ore producers, who are opposed to it and believe affordable energy should be provided instead.

“So, the Minerals Council is fairly conflicted in terms of its structure and we can’t expect the council to particularly carry our voice forward. We have had engagements, or tried to engage, with the ferrochrome producers over this last six months, and with government, but we have not had any constructive engagement. We presented the reports to them but no one has essentially come back with constructive discussions on this,” McAdam said.

“We have written to all of the Ministers involved, asking for engagements. Sometimes it is envisaged that there will be discussions, but they have not been organised. The reason why we have applied for exemption from the Competition Commission is because some of those ideas are not allowed under the legislation. Even to mention them in a forum becomes problematic. They might not be the complete solution to the problem, but we believe they would assist,” McAdam added.

THREAT OF SUBSTITUTION

“One of the key factors that is being under estimated is the ability for other regions to substitute, at higher prices, South African ore,” said Pouroulis.

“Turkey, Kazakhstan and India are, at the moment, not major suppliers of chrome ore because of where the current market prices are, but if you add a tax on top of a South African ore, which typically is a much lower quality, with the metallurgical grade versus a Turkish, or even a Zimbabwean ore for that matter, we believe there’ll be much higher substitution of South African market share by up to 30%, which is a material number. You are talking close to 3.5-million and four-million tonnes of displacement and market share being lost.

“From my perspective, it doesn’t make sense to subsidise an ailing industry and penalise an industry that’s actually grown over the last ten years, that has invested into mining, which, as we know, has not been prevalent over the last decade. Now, they want to potentially jeopardise the future of that part of the value chain that is actually doing relatively well.

“That’s where I find it iniquitous that we haven’t been included in the discussion because we believe that collectively we can support the ferrochrome industry. But we can’t go through those ideas. We haven't even discussed them internally with our forum because of not having a competition exemption, but we believe that collectively we can assist in some shape, form or another, but it wouldn’t necessarily include a tax.

“What we’re saying as this forum is let's just stop, let’s not run away with this idea that we believe is ill-conceived and the benefits overstated, and let’s just debate it holistically, including all interested and affected parties. That’s where we stand today. Whichever government department is responsible, let’s sit around the table, let’s go through the pros and cons of each and every alternative, and let’s find a collective solution,” Pouroulis added.

FERROCHROME RESPONSE

Ferrochrome producers, who are fully behind the imposition of an export tax on chrome ore, have collectively reiterated to Mining Weekly that only 60% to 65% of installed ferrochrome furnace capacity is operating currently owing to the lack of competitiveness of smelters because of high electricity prices.

Also emphasised is their commitment to better efficiencies and competitiveness initiatives, including the self-generation of 750 MW of wind, solar and cogenerated power, support of junior mining development and the encouragement of local coking coal production.

The industry has also committed itself to supporting upstream- and downstream-dependent business, developing new junior anthracite miners, pre-financing already-approved reductant projects, lowering dependence on imported metallurgical coal by encouraging local production, and providing more competitive pricing to local ferrochrome consumers than export customers.

It makes the point that the world’s 85% dependence on South African chrome makes the commodity a strong candidate for domestic value-addition for the benefit of the South African people, who ultimately own it, with mining companies being awarded licences to serve as contractors for laid down periods of time.

At the end of the day, industrialisation and heavy industry generate considerable GDP, bring in considerable foreign income and support a wider range of skills development. The ferrochrome sector, moreover, has existing paid-for infrastructure in place upon which a competitive new advance can take place and advance.

In Richards Bay Alloys' written response to Mining Weekly, Van Heerden drew attention to ChromeSA consisting predominantly of upper group two (UG2) chrome producers, who produce chrome as a byproduct of platinum group metals (PGMs), rather than independent lower group six (LG6) chrome producers, who produce chrome as a primary product.

“Until the last decade, PGM producers’ mining rights did not include chrome. Many of these rights have been subsequently amended to include chrome under the new-order legislation. All of the UG2 chrome recovered from historic dumps was not owned by the PGM miners because the chrome was never included in the original mining rights. This chrome was effectively owned by the South African government, but somehow recovered and sold as South African chrome miners own resource,” Van Heerden stated, referring to the case of Dr Sivi Gounden versus Lonmin Platinum, which Mining Weekly reported on in 2010.

Platinum producers recovered chrome from the historic PGM waste dumps, Van Heerden asserted, with minuscule employment and at low cost.

“They have completely oversupplied the Chinese chrome ore market, selling at well below the cost of traditional chrome mining in South Africa,” Van Heerden added, citing:

- destruction of conventional chrome miner’s profitability, with resultant employment risk at affected operations; and

- the exportation of very low-cost chrome ore feed to the detriment of the South African ferrochrome industry.

This, he said, had opened the door to a large increase in China’s ferrochrome production, despite China hosting no chrome resources within the country.

He countered claims of an export tax being a high-risk intervention by pointing to India’s chrome ore export tax success. The imposition of the tax by India had, he said, encouraged local beneficiation of chrome, enhanced the Indian economy and created additional employment – and even more significant benefit had resulted for Indonesia when it put a complete stop to the export of nickel, the most expensive and the key ingredient in the production of stainless steel, which is also the main consumer of ferrochrome.

“Indonesia implemented a complete ban on the export of nickel-bearing iron-ore. This policy has been a spectacular success as Chinese investment poured into the country. Today Indonesia has a large nickel alloy production as well as two large stainless steel mills, none of which existed three years ago.

“Local beneficiation was the right strategy and led directly to high-value investment, an increased tax base and high-paying jobs. The claim of ChromeSA that international chrome ore producers have excess capacity to displace volumes of South African chrome ore begs the question of why they have not displaced South African chrome ore in the past.

“Because UG2 exports from South Africa have put most other international producers out of business, the production costs of international chrome ore producers are higher than the UG2 Chinese delivered prices.

“International producers need significantly higher sustainable prices to commit the required capital for continued production. The export tax will increase the price to international end consumers; yes, it will assist international chrome ore producers, but this is negligible.

“Let us not forget that 80% to 85% of all chrome ore imported into China comes from South Africa. A shift away from this critical source will be slow and small in the overall market context.

“Reinforcing this point is the fact that the vast majority of the new technology that Chinese smelters have installed is based on a consistent supply of fine ore, such as UG2. The massive sintering lines require the fine ore to be milled even finer, typically to 80% less 75 microns. Changing this is not easy and they will remain dependent on South African UG2 going forward," Van Heerden contended.

UG2 PROFIT NUMBERS NOT DISCLOSED

While publicly listed PGM producers all provided detailed financial reporting, none reported financial detail on UG2 sales: “Is this because it is so insignificant, or is it a hesitation to reveal the cost of UG2 recovery from waste,” Van Heerden asked.

“All in all, the Genesis report, contracted by ChromeSA, has little or no input from the traditional LG6 chrome ore producers. It should therefore be disregarded in its entirety.

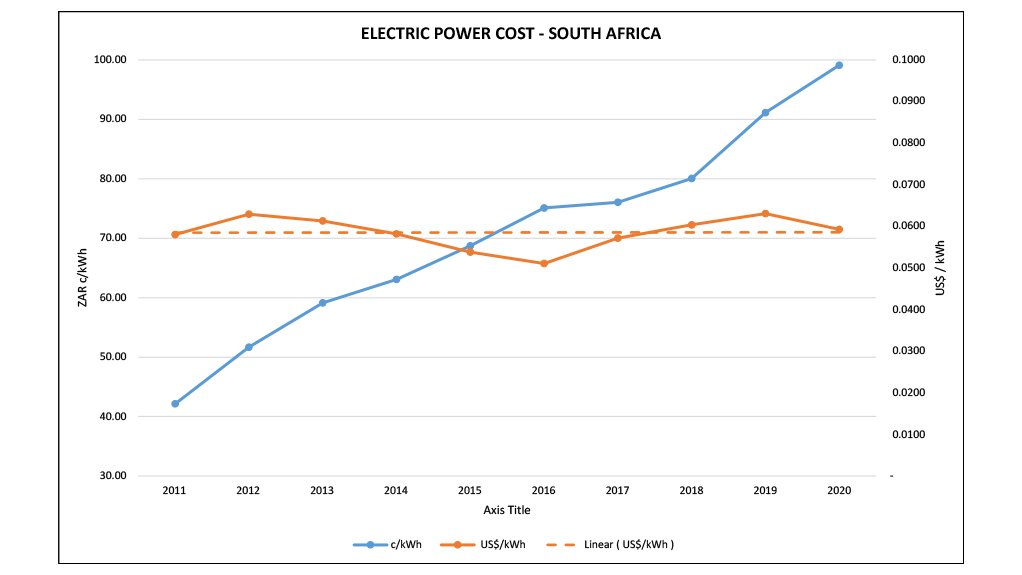

“We have always been upfront in acknowledging that power is, in fact, an issue and there is no denying it. Although the graph (attached above) shows that electricity pricing, in US dollar terms, has stayed flat over the last decade, the prices do make South Africa less competitive than before.

“We believe these will change as Eskom and the government address the power issue. We think the biggest structural change in the next two years in South Africa will be growth in energy with the private sector finally getting on board.

“There are estimates that the private sector will create at least 16 000 MW of generating capacity in the next three to four years and this will help to unleash further investments in industry. We need temporary relief in the form of a tax in order to allow for beneficiation to survive and partner with the private sector as well as Eskom. If one does not implement the tax there will not be an industry that remains viable,” Van Heerden stated.

Kovarsky challenged the assertion that ChromeSA is predominantly made up of UG2 producers and pointed out in a written response that ChromeSA is, in fact, made up of five platinum producers and four LG/MG producers who are reflective of the chrome mining industry.

“Firstly, most chrome is recovered from current PGM production. Secondly, the PGM chrome industry employs approximately 1 280 people. Before the recent rise in PGM prices, the net revenue from chrome comprised almost the entire net revenue of PGM producers and was hence a vital component to their sustainability. The PGM operations which also produce chrome employ over 80 000 people in total,” Kovarsky stated.

“The reference to chrome producers ‘unlocking the chrome floodgates’ is strange as it was a ferrochrome producer that initiated significant exports of chrome ore to China over a decade ago.

“We don’t contest the fact that UG2 has had a dampening impact on chrome prices. However, in 2019 of the 23-million tonnes produced in South Africa, only 6.2m tonnes was UG2. Of the 12.5-million tonnes exported to China in 2019, only 4.8-million tonnes was UG2.

“The reason chrome numbers are not disclosed in PGM annual reports has nothing to do with a reluctance to reveal production costs. Rather, we do not disclose the numbers because they are immaterial to the total costs in the PGM business. In any event the costs of production are well known, all our plants are similar, with a range of costs depending on volume and efficiency.

“Finally, concerns about who this group has had input from are misplaced. We have had input from the members of ChromeSA as well as many independent third party research companies, traders and chrome producers. A number of the research companies have expressed significant concerns about the likely impact of the proposed chrome ore tax on the South African economy,” Kovarsky added.

FERROCHROME COMMITMENTS

In the next 12 months, the ferrochrome industry has collectively committed to:

- removing the distinction between summer and winter Eskom tariffs to allow for improved maintenance planning;

- cogenerating more of its own power to reduce energy cost and load through heat recovery. Already installed are 8 MW of cogeneration and more projects to generate 15 MW have been approved at smelters; and

- continuing to support existing anthracite mining companies.

In the next 12 to 36 months, the ferrochrome industry will:

- introduce 75 MW of additional independent heat recovery projects as well as large-scale 675 MW of wind and solar photovoltaic projects currently planned;

- support new junior anthracite miners; and

- pre-finance projects already approved.

Then in 36-plus months, it will:

- consume competitive long-term Eskom power pricing in South Africa;

- use existing Eskom grid infrastructure as an independent power producer, and look to 200 MW of energy storage opportunities; and

- reduce dependence on imported coke by encouraging local coke production.

Richards Bay Alloys has itself committed to:

- working closely with Swedish Sterling on proven industry-scale Sterling engine technologies to replace 10% of its power needs;

- buying power generated by the new planned gas station in the Richards Bay Industrial Development Zone;

- working on technologies such as pre-heating to further reduce power consumption; and

- working on solar and wind power if it proves viable in the Richards Bay location.

EMAIL THIS ARTICLE SAVE THIS ARTICLE ARTICLE ENQUIRY

To subscribe email subscriptions@creamermedia.co.za or click here

To advertise email advertising@creamermedia.co.za or click here