MACROECONOMIC SLOWDOWN AND PROSPECTS FOR RECOVERY

Introduction

Growth anticipated at time of Budget

At the time of the Budget in March this year, South Africa appeared set to avoid the financial distress and economic reversal that was then confined to Japan and East Asian economies. Lower interest rates, a strengthening of confidence and an acceleration of growth were widely anticipated. The economy was expected to record growth of 3 per cent in 1998/99.

Global financial crisis

Since April, the world economy has been rocked by a deepening banking crisis in Asian economies, a marked slowdown in global trade and massive financial disinvestment from emerging markets.

By some calculations, exchange rate and asset price declines have destroyed more than US$1,5 trillion of financial wealth in the affected Asian countries alone. About the same loss of value has been suffered on the New York Stock Exchange. The Russian economy is in a deep structural crisis, resulting in a debt standstill declaration. Latin American economies are being drawn into the crisis.

Impact on South Africa

South Africa has also been affected. The exchange value of the rand depreciated steeply between May and August this year and the Johannesburg Stock Exchange all-share index lost a third of its value over the same period. Foreign sales of bonds in the third quarter of the year rapidly reversed the net inflows recorded for the first half of the year. Having fallen to below 13 per cent in March 1998, the yield on government stock averaged nearly 20 per cent in August. Money market rates, prime interest rates and home loan rates were six percentage points higher in September than in May, and an unprecedented 16 percentage points higher than consumer price inflation.

Private consumption and retail sales have stagnated, export growth has slowed and business confidence has been severely dented. Although gross domestic product continued to record slight positive growth in the first two quarters of 1998, the economic outlook has weakened. An economic recovery comparable with the growth rates recorded over the 1994-1996 period is now not expected until the second half of 1999.

These developments inevitably impact on the budget for the 1999/00-2001/02 medium term planning period. This chapter provides a brief account of recent international financial developments and the revised macroeconomic outlook for the South African economy. Implications for the budget and fiscal framework are set out in chapter 3.

Background to the Asian crisis

Asian contagion

During the last decade the world has witnessed very strong growth in world trade and international capital flows. These flows contributed to the high rates of growth in many Asian economies, but also to a rapid extension of financial intermediation in an environment in which banking supervision was under-developed. Poor investments, fuelled in part by speculative finance and spiraling asset prices, eventually led to dramatic reversals in several prominent East Asian economies. Private capital outflows in the second half of 1997 resulted in sharp currency devaluations, increases in interest rates and severe declines in stock and other asset markets.

The crisis was sparked by the decline in asset values in Thailand, and pressure on the Thai baht which had become overvalued against the yen. The crisis spread between countries in the region because of trade linkages, the weakness of the Japanese economy and contagion effects operating through capital market sentiment. Having grown by over 5 per cent a year for over a decade, these economies are now shrinking at about the same rate.

Financial vulnerability

The East Asian crisis countries were vulnerable to sudden swings in international capital market sentiment because of the scale of short term foreign currency debt incurred by the private sector. Incentives for foreign borrowing arose from the fixed exchange rate policies adopted by most of these countries as well as from the structure of the financial system and weaknesses in financial regulation. Poor governance structures in the corporate sector also contributed to excessive corporate leveraging, which, together with a deterioration in returns, rendered firms highly vulnerable to interest and exchange rate shocks.

Burden of adjustment

The reversal of high rates of growth in East Asian economies and the impact of economic decline on government services and on employment and earnings of the poor raise important questions about development policies, international finance and the distribution of the burden of adjustment. In responding to these concerns in the Southern African context, the emphasis must fall strongly on protecting services and opportunities for the poor and ensuring that financial contagion does not destroy the livelihoods of working people.

Impact on the world economy

Slowdown in trade and financial flows

The slowdown in the Asian economies, the deepening recession in Japan and a slowdown in China affect growth prospects for the world economy. Commodity prices are low and growth in trade volumes has slowed. Banking failures in Asian economies impact both on fiscal balances in these countries and on international capital flows. Losses made by several prominent investment funds in emerging markets have both raised awareness of financial risks and sharply reversed sentiment towards investment in middle-income economies.

Protracted adjustment

Affected countries have had to implement tighter monetary and fiscal policies, in turn impacting on consumption and trade. It is increasingly apparent that the scale of the non-performing loan problem in the banking systems of East Asian economies is historically unprecedented. A protracted period of financial restructuring and negative or slow economic growth seems likely.

The Asian financial crisis and weakening of stock markets worldwide have increased international concern regarding the transparency of financial markets and the potentially destabilising impact of unchecked financial flows. There are efforts to increase the provision of financial support to countries in difficulties. Improved surveillance and reporting requirements in international capital markets are also under investigation.

Impact on industrial economies

Although moderate growth is expected to continue in the United States and Europe, slower import volume growth is putting pressure on the balance of payments of commodity exporting countries. Recognising the global nature of the economic slowdown, industrial countries are now expected to ease interest rates and cooperate to some extent in seeking greater stability on financial markets.

Initiatives of international financial institutions and the industrial economies may ease the adjustment somewhat, but the global outlook for trade and capital flows remains depressed. Slower world growth will impact on South Africa through both weaker export prices and volumes and a more cautious international investment environment.

Implications for the South African economy

Lower export earnings

About 65 per cent of South Africa’s exports are commodities (including gold) or commodity-related. The deterioration in the demand for commodities thus affects export earnings significantly, weakening both national income and the balance of payments.

Lower oil prices and the currently depressed prices of goods imported from Asia are offsetting pressures on the balance of payments and will contribute to moderating the inflationary impact of the recent depreciation of the rand. However, South Africa’s manufacturing exporters now face more difficult international trading conditions and tough competition from Asian and other countries. The contribution of exports to South Africa’s economic growth is likely to be constrained over the next year or so.

Slower capital flows

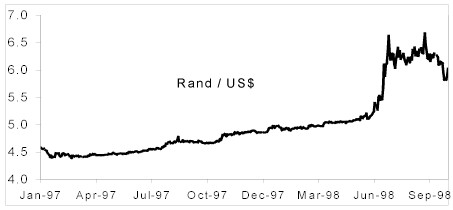

South Africa remains heavily dependent on foreign investment as a result of the low level of domestic savings. Between 1994 and the first quarter of 1998, a total net inflow of capital of R57,4 billion was realised. Since then, long term capital flows have slowed and short term capital has flowed out of the economy, contributing to the depreciation of the rand from an average of R5,05 to the US dollar in April to R6,32 in August and R5,86 at the end of September.

Higher interest rates

High interest rates have contributed to stabilising the rand in September and October, and a recovery of international capital flows in the fourth quarter of the year is possible.

Protecting basic services

South Africa’s social service sectors are well-developed and largely financed through the fiscus. Although government finances have come under pressure in the current financial environment, services remain securely funded and largely unaffected by the downturns in trade and finance. Government recognises that for both long term growth and broad stability of service delivery, basic social services should continue to enjoy sound and stable funding.

South Africa: comparative perspective

Although growth has slowed in the South African economy and foreign portfolio investment has been sluggish, the impact of the changed international environment has been moderate by comparison with many other economies. In East Asian emerging economies growth is now sharply negative, massive outflows of capital have occurred and systemic banking failure remains a serious risk. In Russia, debt obligations have had to be unilaterally set aside and government is unable to meet its pension and other payment commitments.

Underlying strengths

The success of the South African economy in coping with adverse international pressures is partly a consequence of underlying financial strengths:

Policy stability and growth

These factors enhance South Africa’s standing as an emerging economy and underpin longer term growth prospects. However, the risks inherent in the present international context remain considerable. Foreign fund managers are likely to adopt a cautious stance, seeking assurance of a stable policy environment and signs of a recovery of growth before committing to significant levels of reinvestment.

A sound response to currency pressures

Maintenance of sound monetary and fiscal policies has contributed to the adjustment of the South African economy to international pressures.

Monetary & exchange rate policy

In responding to the weakness of the currency, the South African Reserve Bank has provided liquidity to the foreign exchange market from time to time without attempting to defend any particular level of the currency. Interest rates have been raised to encourage foreign investors not to liquidate their holdings, to offset the inflationary impact of the depreciation and to ensure a sustainable position on the current account.

By pursuing fixed nominal exchange rates in a context of capital account liberalisation, many emerging market economies encouraged banks and companies to ignore exchange rate risk, leaving them highly exposed when currencies collapsed.

South Africa has allowed the rand to fluctuate in response to market conditions. This has ensured that companies and banks are very aware of the need to manage exchange rate risk.

Capital market controls

Since 1994 South Africa has progressively lifted restrictions on foreign exchange transactions, thereby contributing to the openness and competitiveness of the capital market.

In the current context of international financial volatility, several countries have attempted to protect their currencies from speculative flows, with varying success. Measures to check capital mobility are difficult to implement and potentially damaging. This is a policy arena in which greater international cooperation is required.

South Africa requires foreign investment to supplement the limited supply of domestic savings. While recognising the importance of extending financial prudential regulations and reporting requirements to foreign exchange transactions, Government remains committed to an open capital market and to the gradual elimination of restrictive exchange controls.

Fiscal policy

South Africa needs to raise domestic savings, while creating further opportunities for foreign investment. Sound fiscal policies will continue to be pursued, aimed at sustaining a moderate and affordable public sector borrowing requirement and encouraging broad-based economic growth.

Investment grade rating

Against the run of expectation, South Africa’s investment grade sovereign credit rating was affirmed by Moody’s Investment Services in October this year.

This reflects a recognition that South Africa’s sound combination of financial and economic policies is a firm foundation for long term growth and development. Amongst emerging markets, South Africa has particular strengths:

Assurance of financial standards

Government will continue to ensure that South Africa maintains the highest standards of regulation, transparency and disclosure in the financial services offered to its people, foreign investors and business enterprises. This assurance underpins the capacity of the economy to respond to the volatility that has proved so destabilising in less developed financial systems.

Real output and expenditure trends

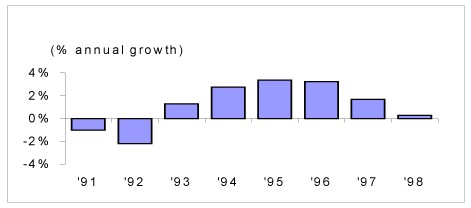

Gross domestic product

Economic growth slowed to just over 1 per cent a year in mid-1997, after three years of GDP growth of about 3 per cent a year. For the first two quarters of 1998, GDP growth was 0,5 per cent and 0,2 per cent annualised.

Figure 2.1: GDP growth

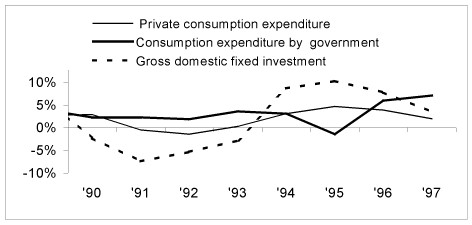

Private consumption expenditure

Growth in real private consumption expenditure slowed down from 3,9 per cent in 1996 to 2 per cent in 1997. In the first half of 1998 real private consumption expenditure slowed further, reflecting high interest rates, growing levels of personal debt and weaker growth in the real disposable income of private households. Strong real wage growth was offset by continued declines in employment in the formal sectors of the economy and an increase in the tax burden of households.

Figure 2.2: Growth in expenditure

General government consumption spending

Real consumption expenditure by general government, comprising personnel remuneration and purchases of goods and services, increased by 6 per cent in 1996 and an estimated 7 per cent in 1997. Government consumption spending has slowed in 1998 and is expected to be about 2 per cent over the year.

Investment

Investment has contributed strongly to expenditure growth in recent years, growing by 7,8 per cent in 1996, 3,5 per cent in 1997 and 7,4 per cent (annualised) in the first half of 1998. The improvement in investment spending in 1998 mainly reflects the expansion of Telkom’s infrastructure investment, facilitated by the enterprise restructuring effected in 1997.

As a percentage of GDP, fixed investment spending increased from 15,5 per cent in 1993 to an average of 17,4 per cent in 1997 and the first quarter of 1998.

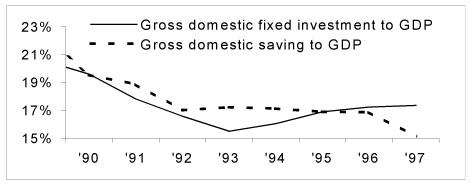

Figure 2.3: Investment and savings

Saving

Inadequate saving remains a structural weakness of the economy. Gross domestic saving declined from 17 per cent of GDP in 1996 to about 15 per cent in 1997 and the first half of 1998. Coupled with the withdrawal of foreign investors from emerging markets over the past year, this keeps interest rates high in real terms and inhibits investment and growth.

Changes in inventories

During 1997 and the first half of 1998 expenditure on GDP has increased faster than output, reflected in steady reductions in the levels of commercial and industrial inventories. The decline in real inventory levels may be explained by several factors:

Once prospects for the economy improve, re-stocking should contribute strongly to a recovery of GDP growth.

International trade and finance

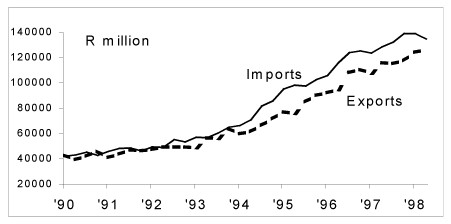

Export and import trends

Export growth has provided an important boost to demand since

1994 and has served to stimulate substantial industrial restructuring. Buoyant demand and industrial investment have fueled strong import growth, however, resulting in a deficit on the current account of the balance of payments. The current account deficit was about 1,5 per cent of GDP in 1997, and is again expected to be between 1,0 and 2,0 per cent of GDP this year.

Figure 2.4: Merchandise imports and exports

Figure 2.5: Balance of payments

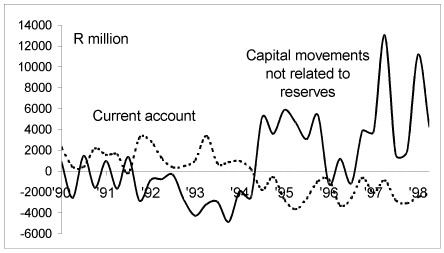

Capital account

Flows on the capital account have been extremely volatile over the last year. In 1997, South Africa experienced a net inflow of capital of R20 billion, considerably exceeding the current account financing requirement. This was followed by a substantial net inflow of capital amounting to R11 billion in the first quarter of 1998 and R4 billion during the second quarter. Since then, a marked outflow of capital has occurred, reflecting the changed investor sentiment to emerging markets.

Foreign reserves

The country’s gross foreign reserves rose substantially in the first half of 1998 as a result of capital inflows and the use of foreign credit lines by the Reserve Bank. The level of net reserves however remains a cause for concern, as foreign investors have become more concerned over the risk of currency depreciation.

In responding to the increased uncertainty on foreign exchange markets this year, the Reserve Bank has continued to meet shortfalls between the supply and demand of foreign currency in the forward market, thereby reversing the considerable decline in its net open forward position recording during 1997 and early 1998. Once stability returns to the foreign exchange market, it is expected that the forward book will return to its longer term downward trend.

Exchange rates

The real effective exchange rate – taking account of the difference between South African inflation and price trends in trading partner countries – depreciated by 8 per cent in 1996 and then appreciated during 1997. Between April and August 1998 the currency came under massive pressure, depreciating by some 20 per cent in real terms before recovering part of its value in September and October. However, exchange rate volatility remains a serious risk in the current distressed international financial environment.

Figure 2.6: Rand-US$ exchange rate

Inflation and money supply

Inflation trend

Inflation in South Africa has been on a declining trend since 1993. Tight monetary policy has ensured that exchange rate depreciation has only had a passing impact on inflation.

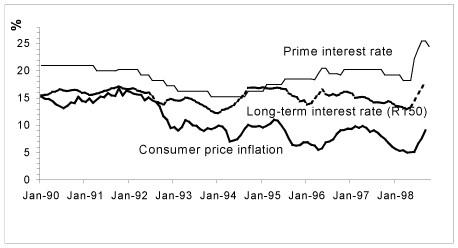

Consumer price inflation averaged 5,7 per cent for the first eight months of 1998, after averaging 8,6 per cent in 1997. Consumer price inflation rose to 9,1 per cent in September, mainly due to the combined impact of the depreciation of the rand and the increase in interest rates on mortgage bonds.

Interest rates

Consistent with the lower inflation environment, interest rates declined during 1997. However, capital outflows, exchange rate depreciation and financial uncertainty put strong upward pressure on money and capital markets in 1998, resulting in unusually high real interest rates. Following improved stability in the exchange rate, interest rates began to decline in October 1998 and are expected to continue to ease during the remainder of the year and in 1999.

Figure 2.7: Inflation and interest rates

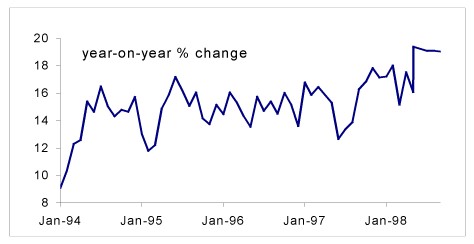

Money supply and credit

Having declined significantly in the early 1990s, the growth rate of broad money (M3) increased rapidly after 1993 and has averaged 15 per cent for the last three years, primarily as a result of private credit growth. This has contributed to the need for a cautious monetary stance.

Figure 2.8: Growth in money supply (M3)

The rate of increase in total domestic credit extension accelerated from 17 per cent in December 1997 to 20 per cent in June 1998 and 22 per cent in August. It is expected that money supply growth and credit extension will slow during the fourth quarter of the year.

Employment and remuneration trends

Employment

Measured formal non-agricultural employment has continued to decline over the past year, decreasing by 1,8 per cent in 1997 and falling further in the first quarter of 1998.

Total employment of 9,1 million recorded in the 1996 census is 75 per cent higher than the recorded non-agricultural aggregate, which leaves considerable scope for uncertainty regarding the overall employment trend. Nonetheless, the deterioration of employment in manufacturing, mining and construction in recent years is a clear sign that structural barriers to job creation remain a serious policy challenge.

Wage trends

Positive real remuneration trends and improved productivity have been marked features of the performance of the economy in recent years. Average real wages have increased by about 2 per cent a year since 1994, both in the public and the private sectors.

Economic outlook

GDP growth

Economic growth is expected to remain subdued in the second half of 1998, before recovering in 1999. As external conditions stabilise, economic growth will strengthen in response to renewed demand and the structural transformation of the economy that is in progress.

Demand

Domestic demand is projected to be weak until the second half of 1999 as private consumption expenditure and private investment are affected by higher interest rates. As inflation and interest rates resume their downward trend, investment and consumption expenditure will strengthen, supported by the impact of demutualisation and increased export competitiveness and renewed foreign inflows.

After a slowdown in 1999, private consumption is expected to grow by 2 to 4 per cent in subsequent years. Gross domestic fixed investment is not expected to grow in 1999, before expanding by 6 to 9 per cent in the following two years.

Balance of payments

Slower growth in domestic expenditure and a depressed rand should in due course lead to a decline in the volume of imports. Whereas commodity export volumes may suffer during the remainder of 1998 in the weak international trading environment, the more competitive rand will provide some relief. Exports of manufactured goods should benefit from improved competitiveness following the depreciation. Overall the current account deficit is anticipated to remain between 1 and 2 per cent of GDP in 1998, rising moderately over the following years.

Exchange rate

The nominal average effective exchange rate is expected to recover somewhat over the coming year before resuming its long run average trend and depreciating by approximately 3 per cent per year.

Large and unpredictable capital movements are likely to be a feature of the global economy in coming months. Sound monetary and fiscal policies should, however, ensure that net capital inflows will continue to exceed the current account deficit over the 1998-2002 period.

Inflation

Consumer price inflation is projected to peak at 9,8 per cent by the end of the year and then decline rapidly towards its 5 per cent trend level during 1999.

Financial stability

Domestic savings will come under pressure in the coming year as households face historically high debt burdens. For this reason, the realisation of a sustained net capital inflow, in the form of both direct investment and portfolio flows, is an increasingly important factor in supporting economic performance. Capital flows not only raise the level of investment, but also provide the liquidity needed in money and capital markets in order for market interest rates to decline.

Risk factors

Although there is every indication that the global financial environment will soon stabilise, the enormous volatility in global markets makes it unusually difficult to predict the outlook for the economy over the next three years.

Several risks to the foregoing outlook should be noted: investment confidence may remain poor; the international financial environment may worsen; and exporters may face increasingly depressed commodity markets.

South Africa’s strengths

However, the underlying strengths of South Africa’s financial structure, moderate debt levels and a sound policy framework are grounds for confidence that the economy will recover strongly in the course of the new year.

Macroeconomic projections

Real GDP growth is expected to improve from about 0,2 per cent in 1998/99 to reach 2 per cent, 3 per cent and 4 per cent over the 1999/00 to 2001/02 period. GDP inflation is expected to fall to 4 per cent in 2001/02 from about 8 per cent in 1998/99.

Table 2.1: Macroeconomic projections: 1998/99 – 2001/02

| Fiscal year: | 1998/99 |

1999/00 |

2000/01 |

2001/02 |

| Gross domestic product (R billion) | 656,9 |

710,2 |

768,1 |

830,8 |

| Real GDP growth | 0,2% |

2,0% |

3,0% |

4,0% |

| Real private consumption growth | -1,0% |

2,0% |

2,6% |

3,8% |

| Real gross domestic fixed investment growth | 0,4% |

-2,0% |

6,8% |

9,0% |

| GDP inflation | 8,0% |

6,0% |

5,0% |

4,0% |

| CPI inflation | 7,5% |

6,0% |

5,0% |

4,0% |

For comparative purposes the above fiscal year projections are converted below into calendar years.

Table 2.2: Macroeconomic projections: 1998 - 2000

| Calendar year: | 1998 |

1999 |

2000 |

2001 |

| Gross domestic product (R billion) | 645,0 |

693,2 |

751,1 |

814,0 |

| Real GDP growth | 0,3% |

1,2% |

3,1% |

4,0% |

| Real private consumption growth | -0,1% |

0,4% |

2,6% |

3,7% |

| Real gross domestic fixed investment growth |

2,3% |

-4,3% |

4,9% |

9,0% |

| GDP inflation | 8,1% |

6,2% |

5,1% |

4,2% |

| CPI inflation | 8,0% |

7,0% |

5,0% |

4,3% |

| Contents | Next |